International index investing works differently from domestic index investing. Before anyone can build an index for “the international market,” someone has to decide which countries count as developed, which count as emerging, which qualify as investable at all, and how much weight each one gets in the final portfolio. None of those questions has an objectively right answer. The three major index providers — FTSE Russell, MSCI, and S&P Dow Jones Indices — have answered them differently for a quarter century, and their disagreements quietly reshape the portfolios of every investor who buys their funds.

The largest single disagreement is South Korea. Korea now has the world’s eighth-largest equity market by capitalization, having recently surpassed the United Kingdom on the back of a semiconductor-led rally. The country is home to Samsung Electronics and SK Hynix, two of the most important companies in the global semiconductor supply chain. FTSE classifies it as developed. MSCI classifies it as emerging. S&P sides with FTSE. Where Korea sits in your portfolio — and how much of your portfolio it represents — depends entirely on which index family is behind your ETFs. Most international investors have never thought about this decision.

The three index families

Almost every international ETF available to U.S. investors is built on top of one of three index families:

FTSE Russell is the index arm of the London Stock Exchange Group. FTSE classifies South Korea as a developed market and has done so since 2009. Vanguard’s international ETFs follow FTSE methodology. Schwab’s flagship international fund does as well.

MSCI is the largest of the three by institutional assets and is the standard benchmark most pension funds and endowments measure against. MSCI classifies South Korea as an emerging market and has held that view since 1992. iShares uses MSCI methodology for its core international lineup. Avantis and Dimensional do too.

S&P Dow Jones Indices runs the S&P 500 and is the third major provider. S&P has classified South Korea as a developed market since 2001. State Street’s SPDR portfolio international funds follow S&P methodology.

Two of the three providers say developed but one says emerging.

Four emerging-markets ETFs, four very different Korea exposures

Look at the four most widely used emerging-markets ETFs in the U.S. market and the consequences of these classification choices become clear.

| ETF | Issuer | Index | Korea Weight |

|---|---|---|---|

| IEMG | iShares (BlackRock) | MSCI EM IMI | 15.4% |

| VWO | Vanguard | FTSE Emerging | 0% |

| SPEM | State Street SPDR | S&P Emerging BMI | 0% |

| AVEM | Avantis | MSCI EM IMI (active) | 15.6% |

Korea weights as of recent fund disclosures. AVEM weight as of 3/31/2026 per issuer fact sheet.

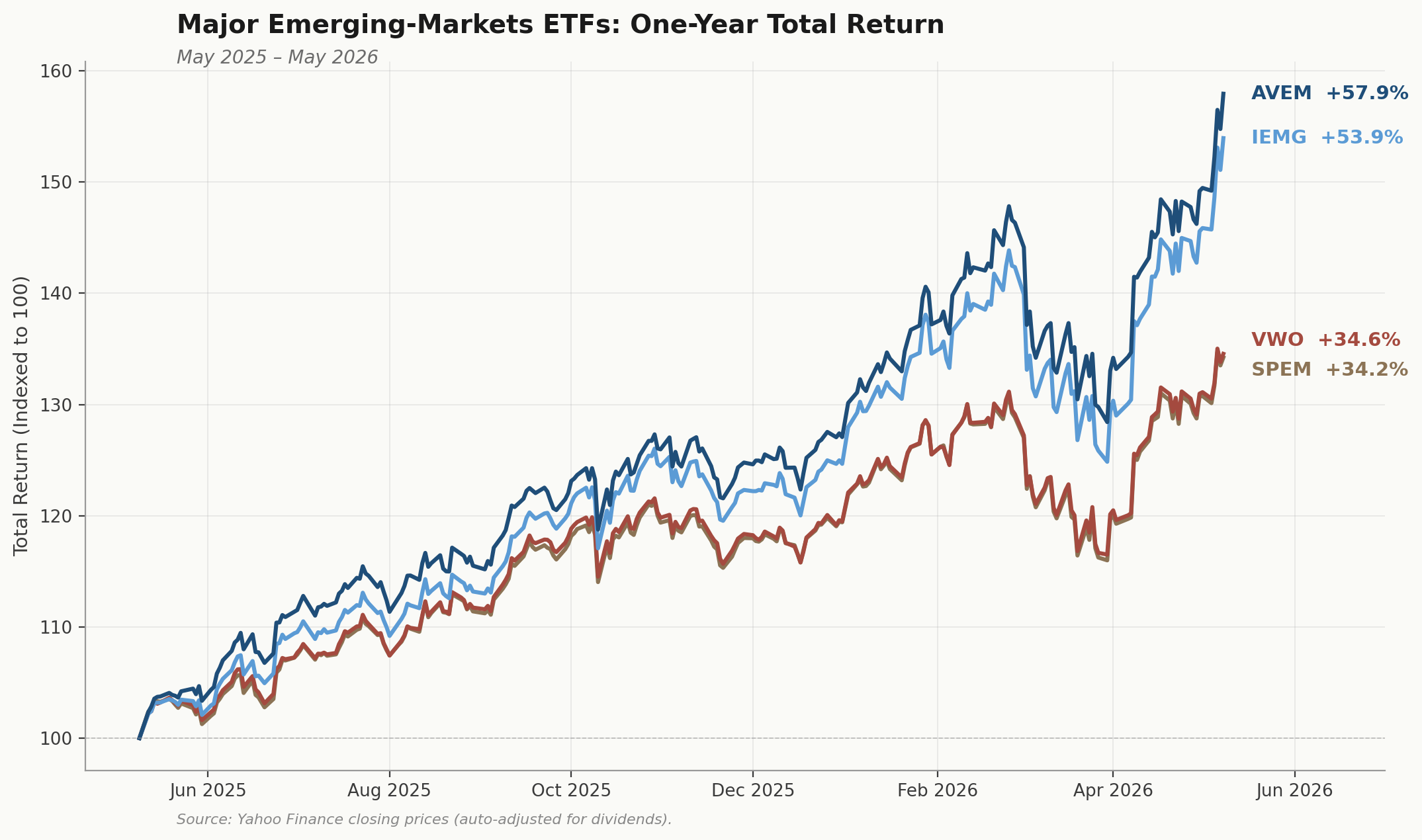

Two of the four major emerging-markets ETFs hold zero Korea. SPEM and VWO both follow indexes that classify Korea as developed, so neither owns Samsung Electronics, SK Hynix, or any other Korean stock. An investor who bought either fund expecting “broad emerging markets exposure” was structurally absent from the entire AI memory cycle.

IEMG sits in the middle. The MSCI EM IMI index that BlackRock tracks places Korea at roughly 13% of the fund. That weight has powered IEMG’s recent performance, since Samsung and SK Hynix have been among the largest contributors to MSCI emerging-markets returns since 2024.

AVEM is the highest-Korea fund of the four despite being the only one that’s actively managed. Avantis benchmarks against MSCI EM IMI but tilts the portfolio toward smaller-cap, value, and high-profitability stocks. Korean memory names, which trade at low book multiples and generate strong returns on capital, get systematically overweighted by the model.

The performance gap over the trailing twelve months ending May 2026 made the math visible:

AVEM (Korea 15.6%) returned +57.9%. IEMG (Korea 13.3%) returned +53.9%. VWO and SPEM, both with zero Korea exposure, returned +34.6% and +34.2% respectively. The gap between the highest-performing fund (AVEM) and the lowest (SPEM) was 23.7 percentage points. All four are marketed as broad emerging-markets ETFs.

Conclusion

Passive portfolios are full of active decisions. Those choices are made by the index provider before the ETF is built, and the investor inherits them whole.

Passive investing is one of the most powerful tools available to long-term investors. It just isn’t as automatic as it looks the moment you cross the U.S. border.

This commentary is provided for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security. ETF holdings, index weights, and performance figures cited are as of dates referenced and change over time. QuantWealth Advisors LLC is a fee-only registered investment adviser.