MercadoLibre, Sea, and Coupang are the dominant online retailers in their home markets, the closest equivalents to Amazon in Latin America, Southeast Asia, and South Korea. Together they serve hundreds of millions of customers across the developing world. Yet none of the three appears in the major emerging-markets indices that most investors rely on for exposure to those economies. The reason has little to do with the quality of the businesses. It is a function of where each company is incorporated and where its shares are listed.

The three companies

- MercadoLibre is the largest e-commerce company in Latin America and the region’s leading digital-payments provider. Its marketplace operates across 18 countries and holds the number-one position in its biggest markets, Brazil, Mexico, and Argentina. Its fintech arm, Mercado Pago, operates in eight countries and leads in active users in Argentina, Chile, and Mexico, ranking second in Brazil. Revenue reached roughly $29 billion in 2025. The company was founded in 1999 by Marcos Galperin, who served as chief executive until January 2026 and now leads it as executive chairman.

- Sea Limited runs Shopee, the largest e-commerce platform in Southeast Asia, with more than half of the region’s online retail volume and the leading position in Indonesia, its single biggest market. It operates across Singapore, Indonesia, Malaysia, Thailand, Vietnam, the Philippines, and Taiwan, as well as Brazil, alongside the Garena games business and the Monee digital-finance arm. Sea was founded in 2009 by Forrest Li, who remains its chairman and chief executive.

- Coupang is the largest e-commerce company in South Korea, often called the “Amazon of Korea,” where it generates close to 90 percent of its revenue. It is the fastest-growing entrant in Taiwan, where its fulfillment network already reaches about 70 percent of the population, and it owns the global luxury platform Farfetch. Revenue exceeded $30 billion in 2024. Coupang was founded in 2010 by Bom Kim, who retains control of the company through a dual-class share structure.

All three earn the overwhelming majority of their revenue in developing markets. By any economic measure, they are emerging-market businesses.

Built to compound

These are, in their structure and behavior, the public-market versions of the companies investors increasingly reach for in private markets. Founder-controlled and run for long-horizon growth rather than near-term distributions, they reinvest heavily and compound capital over many years. That profile, a committed founder with aligned ownership, a large and underpenetrated market, and the patience to build through cycles, is much of what draws institutional capital into venture capital and growth-equity funds in the first place. Consider what a US equity index would have done to its investors had it excluded Amazon over the past two decades; the major emerging-markets indices apply that same kind of exclusion to the leading companies here. MercadoLibre, Sea, and Coupang show that the profile exists in liquid, publicly listed form. An investor who accepts high fees and multi-year lock-ups to own founder-led compounders privately can find a closely related exposure in public markets, though only by looking past the index that is meant to represent those markets.

Why the indices exclude them

Index providers assign each company to a single country based mainly on where it is incorporated and where its shares are primarily listed, not on where it does business.

- MercadoLibre is incorporated in Delaware and headquartered in Uruguay, and its shares trade on Nasdaq. Its country of origin, Argentina, is classified as a standalone market rather than a full emerging market.

- Sea is incorporated and headquartered in Singapore, which the major providers classify as a developed market, and it lists on the New York Stock Exchange.

- Coupang is incorporated in Delaware, headquartered in Seattle, and listed on the New York Stock Exchange.

In each case the company’s legal and listing footprint points away from any emerging-market country index, so it is left out. By contrast, Nu Holdings, the Brazilian digital bank, is included in the MSCI and S&P emerging-markets indices despite its Cayman incorporation and New York listing, because it also maintains a local Brazilian listing that anchors it to Brazil. The three companies here maintain no comparable local listing.

A pattern, not a one-off

The exclusion of these three is not a set of isolated quirks. It reflects how many of the most successful emerging-market technology companies are built and financed.

Founder-controlled companies in the developing world frequently choose to incorporate in Delaware or the Cayman Islands and to list in New York rather than on their home exchange. The reasons are practical: access to deeper pools of capital, a broader base of global investors, familiar legal and governance frameworks, and, in many cases, dual-class share structures that let founders keep control after going public. MercadoLibre, Sea, and Coupang each followed a version of this path, and Coupang’s dual-class structure is a direct example of founder control written into the listing itself.

Those same choices are what remove the companies from the emerging-market indices. The classification rules are built around where a company is domiciled and listed, not around where it operates or where its growth comes from. As a result, the methodology tends to underweight the segment that best represents the modern emerging-market economy: the digital, consumer-facing, founder-driven businesses that have grown the fastest.

The effect is that a passive emerging-markets allocation leans toward the established part of these economies, the large banks, commodity producers, incumbent telecoms, and export manufacturers, while under-representing the entrepreneurial growth segment built by founders who listed abroad. An investor who buys a broad emerging-markets fund expecting to own “emerging markets” is, in practice, owning a version tilted away from its most dynamic companies. Because each new generation of founders tends to follow the same US-listing playbook, the gap is more likely to widen than to close.

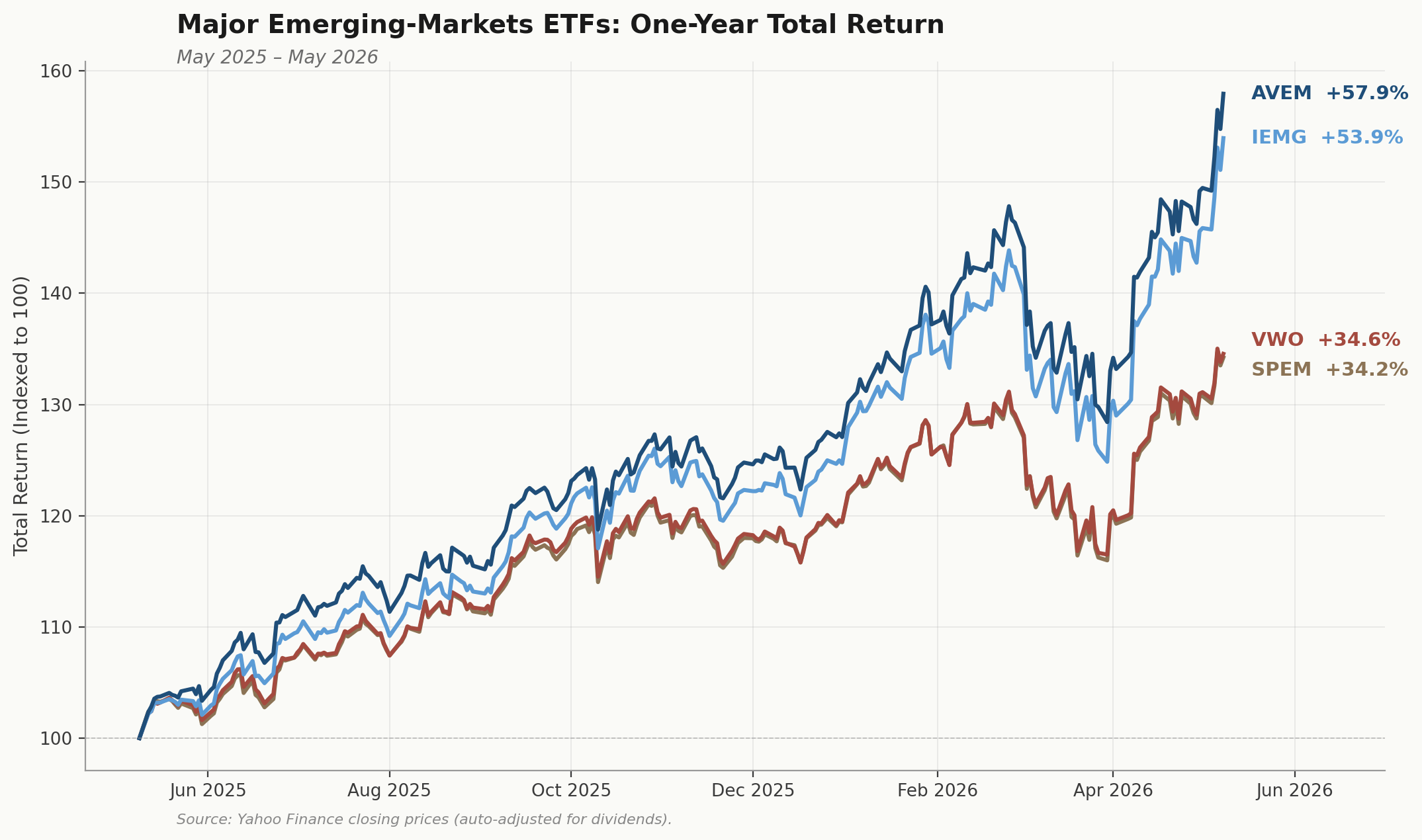

The performance record

The companies excluded by this methodology have produced a wide range of outcomes, which is itself part of the point.

Measured from each company’s IPO, a $10,000 investment in MercadoLibre at its first traded price would be worth about $608,700 today, and the same amount in Sea would be worth about $53,700. The three emerging-markets index funds returned roughly $22,000 to $26,000 over the same periods. Coupang shows the other side of the distribution: $10,000 became about $3,600, a loss that index investors avoided.

What it means for a portfolio

The practical implication is straightforward. Exposure to these businesses has to be added deliberately, because no broad emerging-markets index will provide it. For a portfolio meant to capture the emerging-market consumer and technology theme, the gap is worth identifying explicitly, sizing as an active decision, and evaluating on the fundamentals of each company rather than leaving it to a classification rule written for a different purpose.

Understanding what an index excludes, and why, is a prerequisite for deciding whether that exclusion is one you would choose.

QuantWealth Advisors LLC is a registered investment adviser. This material is for informational and educational purposes only, reflects opinions as of the date of publication, and is not investment, legal, or tax advice or a recommendation to buy or sell any security. Past performance does not guarantee future results. Index membership and fund holdings are as of June 2026 and are subject to change. The firm and its clients may hold positions in the securities discussed.