Secondary Evergreen Private Equity (PE) funds have expanded rapidly in recent years, offering investors diversified access to seasoned private equity investments with semi-liquid structures and faster deployment profiles. In a previous blog post, I discussed why investing early in these funds can be particularly advantageous: Why Investing Early in Secondary Evergreen PE Funds Is So Powerful.

As more investors consider Evergreen secondary funds as strategic long-term allocations rather than tactical short-term opportunities, an essential question arises:

Do Secondary Evergreen PE funds demonstrate durable long-term performance?

The challenge is that most of these funds are relatively new, with limited operating histories. As a result, understanding their long-term potential requires analyzing performance patterns across the small set of managers with track records long enough to evaluate.

Performance Summary of the Oldest Evergreen Secondary Funds

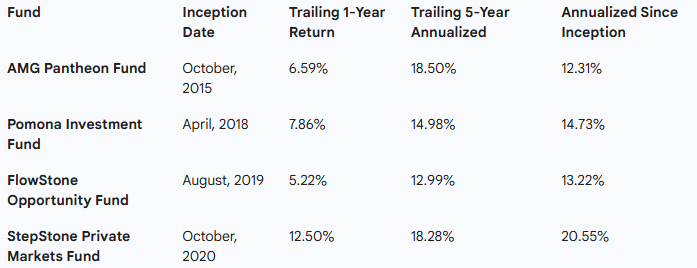

Below is a consolidated snapshot of four of the longest-running Evergreen Secondary PE funds. Stepstone Private Markets Fund is the newest among them, having just passed its five-year anniversary.

These figures capture each fund’s trailing 1-year return, 5-year annualized return, and since-inception annualized performance.

Summary Performance Table

What the Data Suggests

When comparing long-term and short-term results across these funds, several patterns emerge:

- The trailing 1-year average return is meaningfully lower than the trailing 5-year return across these funds.

Specifically, the trailing 1-year performance is 8.15% lower than the trailing 5-year annualized figure. - The trailing 1-year performance also trails the since-inception annualized numbers by an average of 7.16%.

- Long-term returns appear strong, but a portion of this strength likely reflects early-period conditions—particularly wider secondary discounts available in 2020–2021 that later compressed, producing significant mark-ups.

- Recent performance has softened across the category, suggesting that the early tailwinds should not be assumed to persist indefinitely.

Given the small number of funds with multi-year histories and the relatively short existence of the Evergreen secondary structure itself, forming definitive long-term conclusions remains difficult.

Some funds continue to raise assets rapidly, benefiting from scale, sourcing, and flow advantages. Others are experiencing slower inflows, which can affect deployment pace, liquidity profiles, and future performance. These differences make cross-fund comparison challenging.

Possible Reasons for Recent Underperformance

- Early returns were boosted by unusually large secondary discounts Growing AUM and larger discounts produced outsized gains that are unlikely to repeat

- Private equity performance has slowed broadly PE distributions have declined, transaction volumes remain lower, and valuations have been more muted. Evergreen funds holding secondary positions naturally reflect this environment.

- Not all discounted secondary deals were high quality Some managers purchased discounted interests for which the underlying fundamentals later proved weak. Some of the larger discounts led to the funds having weak assets.

- Secondary discounts today are much tighter With fewer distressed sellers and more capital pursuing secondary opportunities, the pricing advantage enjoyed by these funds early on has largely dissipated.

Conclusion

Evergreen Secondary Private Equity funds have delivered strong long-term performance to date, but a meaningful portion of those returns was driven by unique early conditions—namely wide discounts and robust inflows. More recent results show a noticeable slowdown, reflecting both market-wide private equity headwinds and the natural maturation of the strategy.

While it is still too early to draw firm conclusions about long-term durability, investors should monitor the category closely, focusing on discount discipline, sourcing quality, AUM stability, and manager selection as key drivers of outcomes going forward.

Disclosures

This content is for informational purposes only and does not constitute investment, tax, or legal advice. Past performance is not indicative of future results. Private equity and secondary investments involve substantial risks, including loss of principal, illiquidity, long time horizons, and reliance on underlying manager valuations. Evergreen private equity structures vary significantly across providers. Investors should carefully review offering documents and consult qualified professionals before making investment decisions.